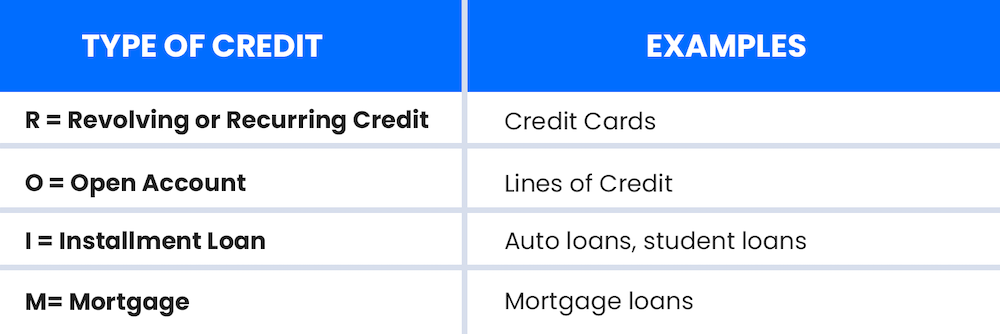

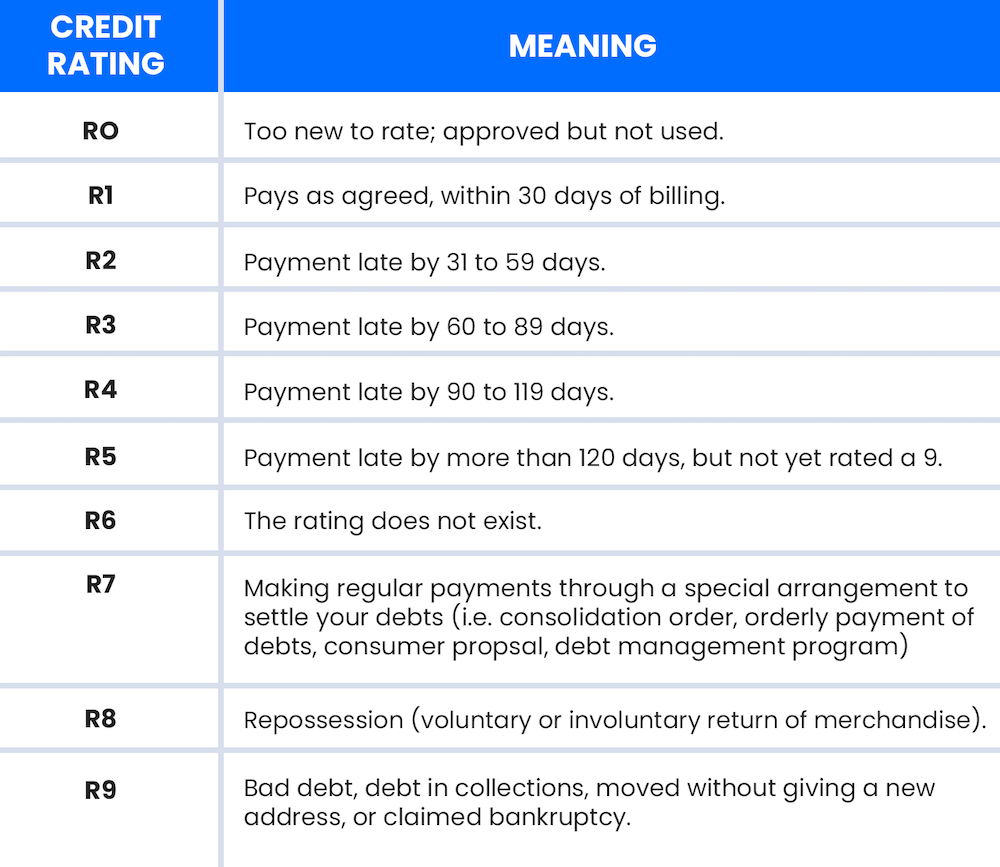

Each account shown on your credit report will have a rating, which reflects the type of credit and the current payment status of the account. The type of credit is indicated by a single letter and the payment status will be a number between 0 and 9. This scale is NOT linear - the numbers simply describe the current payment status.

The tables featured here explain the meaning behind each letter and number for a credit rating.

If you've ever used a credit card, have a cell phone plan or taken out a personal loan, then you've got a credit score.

Your credit score is calculated by credit bureaus that convert information on your credit report to a number based on a formula called the “FICO formula.” Your credit score will be a number between 300 and 900.

Here are the factors that make up your credit score and a percentage indicating how important they are when it comes to calculating your score.

Generally, a credit score approaching 700 or above is looked at favourably by lenders, meaning you probably won’t be turned down for credit or a loan, and the interest rate will likely be reasonable. If your credit score is 800 or above, you’re in excellent shape.

According to FICO, for people with “normal” credit profiles, payment history and credit already used make up 65% of your credit score.